Be it an investment or a loan, interest rates determine the total earnings or borrowing cost, respectively. Usually, individuals consider two types of rates – simple interest and compound interest rates.

Take a look at the brief overview of simple and compound interests, ways to calculate them, and other important details.

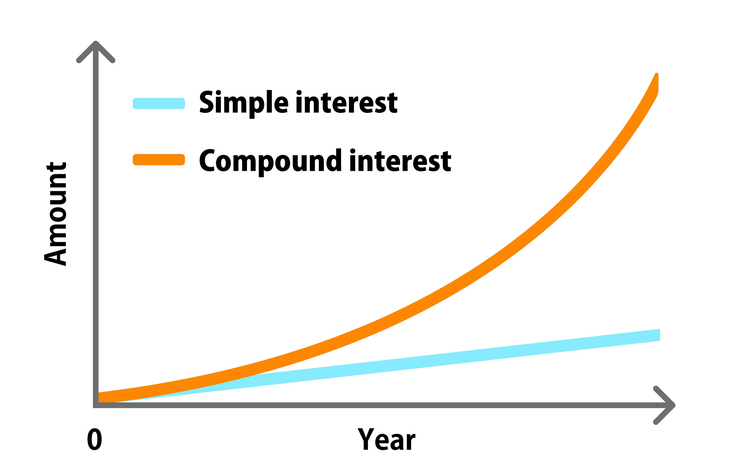

An overview of simple interest and compound interest rates

Both simple and compound rates determine the cost of borrowing a loan. A lender levies an interest rate on a loan amount for utilizing the borrowed money for a fixed period.

A compound rate has the potential to help investors earn more returns than a simple interest income. It applies to the total loan amount and interest as well. Often a financial institution determines how often the interest will be compounded.

It can compound quarterly, monthly, daily, annually or half-yearly. Financial institutions use this on investments such as mutual funds, fixed deposits.

Now, let’s move ahead with the calculation using a compound and simple interest formula.

How to calculate a simple interest rate?

Calculating simple interest beforehand will help one to compare and avail better interest rates for loans. One can compute interest payables on loans by using this simple formula:

SI = P*I*N

Whereas,

SI = Simple interest

P stands for Principal amount

I is equivalent to interest rates for a given period

N is tenor

For a simple understanding, let’s take an example:

Example 1

An individual borrows a loan of Rs.50,000. The tenor is 60 days, and the interest rate is 5% per year. The calculation is as follows:

Principal amount = Rs.50,000

Interest rate= 5% per year

Tenor = 60 days

Total interest payable = Rs. 410.95

Note that the more is the principal or loan amount, the more individuals pay the interest. However, selected NBFCs such as Bajaj Finserv offer a high-value personal loan at a nominal interest rate to an eligible candidate.

Also, the financial institution extends pre-approved offers, which streamlines the application process. These offers are available on a host of financial products like personal loans, business loans, etc. Willing applicants can check their pre-approved offers by submitting their names and contact details.

Alternatively, individuals can use a personal loan calculator. It eliminates the effort to calculate the total amount of payables manually. Besides, they should also know how the compound interest works.

How to calculate a compound interest rate?

Individuals can calculate a compound interest using this formula:

A=P(1+r/n)^(n*t)-1)

Where the A stands for compound interest

P = Principal amount

n = the number of compounding tenor

r = interest rate

t = duration

let’s take a simple example to understand how compound interest works

An individual invests Rs.10,000. The tenor is 5 years, and the interest rate is 10%. Thus, the calculation is as follows:

A = 10000*((1+10%)^(5)-1) = Rs. 6,105

The total accumulated corpus at the end of tenor will be Rs.16,105. Similarly, the simple interest income is Rs.15,000 given the similar investment and tenor. Ultimately, there is a difference between the simple and compound interest of Rs.1,105.

What is meant by the power of compounding?

Compounding denotes reinvestment of earnings. Accordingly, initial investment and reinvested incomes grow and multiply at a faster rate. Interest will be higher depending on the frequency of compounding. For a better understanding, let’s take an example:

An individual’s total investment is Rs.10,000. The interest rate is 10% per year and tenor 5 years. The compounding period is 2 years.

Hence, the total income at the end of the tenor is Rs. 16,289. Therefore, an individual earns an additional income of Rs.183. (compared to Rs.16,105).

Read More: Story of OiO Travel Chief Executive Rajeev Ranjan

Thus, this sums up the power of simple and compound interest rates. Not considering the interest type is one of the things to avoid while taking personal loans. Correct knowledge about both is essential to make an informed decision on investment or borrowing.

2 Comments

Pingback: Does Your Financial Planning at 32 Include Individual Health Insurance

Pingback: How Wireless Panic Alarms Can Help You Get Out of an Emergency