Input Tax Credit under GST is the important pillar of the GST structure in India.

Claiming of eligible ITC is important for businesses but claiming ineligible ITC may land the businesses in trouble.

Even if the businesses end up claiming some ineligible ITC, there’s a simple process to reverse this ineligible ITC in the GSTR-3B return. We will discuss the same in the later part.

In this short article, we have defined& explained the concept of ITC reversal under GST and simplified the process with an example.

Input Tax Credit under GST Reversal | Meaning explained

There are certain pre-requisites that a taxpayer or a GST registered business need to fulfill to avail the eligible GST Input tax credit:

- Pending payments with your supplierare settled within six months (180 days) from the transaction date.

- The input purchases & the capital goods on which ITC is to be claimed should be used for the business purpose ONLY. These goods should NOT be used for any personal consumption.

- The input purchases or capital goods should NOT be further used for supplying the exempted goods.

These are the three basic conditions that every business should fulfill before availing any Input tax credit in the input purchases.

However, most of the businesses fail to satisfy some or all of these conditions and end up claiming ineligible ITC.

So, how can a business reverse the ineligible ITC ?

The answer is simple, taxpayers shouldREVERSE their ineligible Input Tax Credit while filing their GSTR-3B returns.

We’ll discuss the steps in the later part of the article.

Ineligible ITC reversal with example

Following are the two essential rules to focus on for ITC reversal process:

- Rule 42 of CGST Act, 2017 (ITC Reversal on Inputs)

- Rule 43 of CGST Act, 2017 (ITC Reversal on Capital Goods)

- Rule 42 of the CGST Act, 2017

This rule is concerned with the determination of ITC on the input services and their reversal.

Let us submit an example before you to express the working of this rule in ITC reversal process.

Example:

Following are the details of ‘Jethalal Electronics’ for the month of November 2021 for the supplies made in Pune. Maharashtra.

| Heads | Details |

| Total ITC Available (T) | ₹3,30,000 |

| ITC on supplies (personal consumption) (T1) | ₹10,300 |

| ITC on inputs (for exempted supplies) (T2) | ₹19,000 |

| Blocked credits (e.g. GST on Personal travel fare) (T3) | ₹4,400 |

| ITC on supplies that are taxable (T4) | ₹ 1,60,000 |

| Exempt supplies (E) | ₹ 3,10,000 |

| Total turnover of the firm ‘Jethalal Electronics’ (F) | ₹35,00,000 |

From the table,

ITC according to the credit ledger of this business will be:

(C1) = T – (T1+T2+T3);

C1 = 3,30,000 – (10,300+19,000+4,400)

Therefore, C1 = ₹2,96,300;

Common Credit (C2) = C1 – T4

C2 = 2,96,300-1,60,000 ,

C2 = 1,36,300;

Now, to calculate ITC towards exempt supplies from common credit,

ITC towards exempt supplies from common credit (D1) = (E/F) × C2

D1 = (3,10,000 ÷ 35,00,000) × 1,36,300

D1 = 12,072;

Now,

ITC for non-business supplies out of common credit (D2) = 5% of C2

D2 = 5% of 1,36,300

D2= 6,815;

Now,

Remaining eligible ITC from the common credit (C3);

C3 = C2 – (D1 + D2)

C3 = 1,36,300 – (12,072 + 6815)

C3 = 1,17,413

Hence, for the firm ‘Jethalal Electronics’ we can conclude that, out of total available GST Input Tax Credit:

| Amount | Action |

|

C3 (Rs. 1,17,413) & T4 (Rs. 1,60,000)

|

Credited to electronic ledger |

|

D1 (12,072) & D2 (6,815) |

This ITC of 12,072 + 6815 = 18,887 to be reversed in GSTR-3B |

In this example, the ineligible ITC claimed by the business was Rs. 18,887 & should be reversed by the business in the upcoming GSTR-3B return.

Reversing ineligible ITC based on the Rule 43 of CGST Act, 2017

In order to reverse the ineligible ITC availed on the capital goods, the taxpayers should satisfy the following conditions:

- The ITC to be reversed is availed for the purchases used for non-business purposes.

- The GST Input Tax Credit is related to the capital goods utilized for supplying supplies other than exempt supplies, including the nil-rated supplies.

Reversing your ineligible ITC with GSTR-3B

Businesses can easily reverse their ineligible ITC in their GSTR-3B return.

Businesses must observe due diligence while claiming any Input tax credit. In case, if a business claims any ineligible ITC, it should soon reverse this ineligible ITC in the GSTR-3B returns.

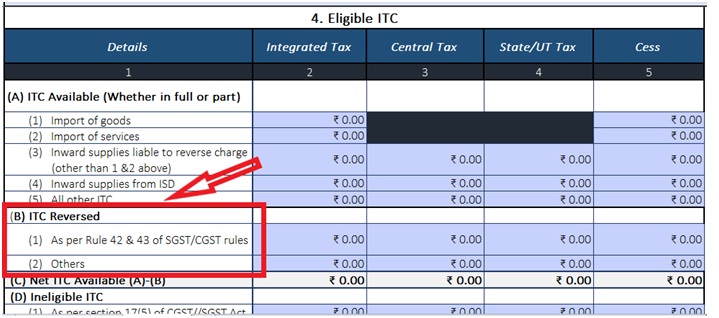

GSTR-3B return form holds a separate column where you can provide the details of all the ineligible ITC availed by you in a month.

There are two important headers in this column as highlighted in the image above:

- AS per Rule 42 & 43 of SGST/CGST rules

- Provide the details of the GST Input Tax Credit claimed on inputs of products/services which are partly used for business & partly for non-business purpose.

- When the input supplies of the business includes any nil-rated supplies orexemptgoods, then the ITC reversal on them is required & these details are to be furnished in this column.

- Others

- Under this header, details of other GST Input Tax Credit should be mentioned.

- These ‘Other ITC details’ can be based on the purchase registers or books of accounts of the business.

NOTE:

CBIC has time and again clarified that the businesses must refer to their GSTR-2B for finding the details of their eligible Input Tax Credit for a given month.

GSTR-2B must be used as an authoritative & definite source to find the details of your eligible Input Tax Credit under GST.

In a nutshell

Claiming of ineligible Input Tax Credit under GST can attract a GST audit by department and also lead to cancellation of the GST registration of the business.

Hence, businesses must observe due diligence while claiming their Input Tax Credit.

Read More: Float Protocol Raises $1.2M from Strategic Partners like MCV and LAO to Create a Truly Decentralized, Non-dollar Stablecoin

In case, if the businesses have claimed any ineligible Input Tax Credit for the month, it has to be reversed in the GSTR-3B by providing all the details of this transaction.

In this article, we discussed simple ways to reverse ineligible ITC claimed with an illustrative example to understand.

1 Comment

Pingback: Everlasting Benefits of Opting for the Best Web Content Writing Services